Luna - The Fat Octopus Protocol

A look into how the Luna token derives and captures value from the Terra blockchain and Terra ecosystem.

NB: This post is an excerpt from a longer investment thesis for the Luna token and the Terra ecosystem.

Disclaimer: This is not financial advice and the author of this post owns the Luna token.

Terra’s vision is grand and ambitious, it attempts and is making great strides to upend not only the traditional financial industry but the new world of financial technology.

Background & Protocol Mechanism

Terra is a decentralized financial infrastructure and blockchain protocol that supports a basket of native, fiat-pegged stablecoins which are algorithmically stabilized by its native cryptoasset, Luna. Terra was founded by the Terraform Labs (TFL) company in 2018.

Terra Blockchain

Terra can be considered an application-specific blockchain as it was designed for a specific purpose in mind, a decentralized financial platform rather than a general purpose blockchain like Ethereum. The Terra blockchain was built using Cosmos SDK and using Tendermint for delegated Proof-of-Stake consensus. The Tendermint BFT (byzantine fault tolerant) consensus algorithm and BFT engine is a solution that packages the networking and consensus layers of a blockchain into a generic engine, allowing developers to focus on application development as opposed to the complex underlying protocol. The Cosmos SDK is a generalized framework that simplifies the process of building secure blockchain applications on top of the Tendermint BFT.

Terra Stablecoins

The basket of native and algorithmic Terra stablecoins are pegged to various fiat currencies (USD, KRW etc.). Terra achieves price-stability by algorithmically adjusting its supply according to fluctuations in demand (video explainer).

For example, increased demand in TerraUSD (UST) will manifest in an increase in the volume of transactions and price of UST. So that the price of UST does not deviate from its peg, the USD, Terra must apply balancing, reactionary forces. In this scenario, the protocol must expand the supply of UST to compensate for the extra demand. This is achieved by natural efficient market forces, through opportunistic and independent arbitrageurs who can extract risk-free profit by minting UST that is worth more than its peg and then selling it, banking the difference.

To mint 1 UST the protocol needs to burn $1 worth of the Luna token. This mechanism of burning and in essence, recapturing the value in Luna is called seigniorage and represents the value gained from minting Terra stablecoins.

In a contractionary scenario, fall in demand of UST results in an equivalent drop in the price and requires the supply to be decreased to maintain the peg. The drop in value from decreased demand is absorbed by the Luna token, diluting its supply and transferring value from the Luna collateral to raise the price of UST. This scenario of decreased demand for Terra stablecoins is value-dilutive to the Luna token and its holders.

Luna

Luna is the native governance and staking token which serves its purpose as collateralizing the mechanisms that secure the price-stability of Terra stablecoins and influence the incentives of validators.

Luna’s primary function is to secure the integrity of the Terra network by locking value within the ecosystem through staking. Staking rewards are provided in order to incentivize long-term stability and value within the network. These rewards are first distributed to the validators who can take a varying commission rate (determined by the validators themselves) before they are then distributed and withdrawn by delegators. Staking rewards are issued proportionally to the size of the stake and come from three primary sources (gas (compute fees), taxes and seigniorage rewards) and one additional variable source (airdrops).

Taxes are used as a stability fee where the protocol charges a percentage transaction fee ranging from 0.1% to 1%.

Seigniorage Rewards

Validators participate in the Luna exchange rate oracle process and win rewards from the seigniorage pool every time they vote within the reward band, proportional to their stake.

When Luna is burned to mint new Terra stablecoins, the amount of Luna burned is “seigniorage”. Every treasury epoch (1 week) a portion of the seigniorage is routed to:

fund the community pool, a keyless wallet controlled by Luna governance to fund various initiatives within the ecosystem

fund the reward pool, which is distributed over a 1 year period

With the recent TIP 43 proposal passing, seigniorage rewards will no longer be routed to fund the reward pool and as such will not be used as a dividend for staking rewards.

Value Proposition

Three primary narratives exist for the investment thesis behind the Terra blockchain and its ecosystem, the Luna token and how it effectively derives value from the growth of the network, and ultimately the vision and execution of the founding team.

1. Value Capture: The Fat Octopus Protocol

The Fat Protocol Thesis

The “Fat Protocol” thesis, developed by Joel Monegro in 2016 is a compelling thesis behind the proportionally large amounts of value (“fat”) captured by the protocol layer within a blockchain relative to the application layer. Joel argues that whilst the previous generation of shared protocols such as TCP/IP, HTTP, SMTP etc. produced immeasurable amounts of value, most of it was captured and re-aggregated on top at the applications layer, such as Google and Facebook. Joel’s primary argument is that due to positive feedback loops between utility, speculation and innovation, the protocol layer will grow faster than the combined value of the applications built on top of it.

In his own words: “the market cap of the protocol always grows faster than the combined value of the applications built on top, since the success of the application layer drives further speculation at the protocol layer. And again, increasing value at the protocol layer attracts and incentivizes competition at the application layer. Together with a shared data layer, which dramatically lowers the barriers to entry, the end result is a vibrant and competitive ecosystem of applications and the bulk value distributed to a widespread pool of shareholders. This is how tokenized protocols become ‘fat’ and its applications ‘thin’.”

Almost 5 years later, this thesis is a widely recognized and evidence backed understanding for why and how blockchains and most notably Ethereum captures value.

Revenue Sharing (Staking Rewards)

Arguments about whether cryptocurrencies or crypto-assets are a form of money and not equity are so yester-year. Most of the rhetoric about not “wanting” to be an equity stems from fears about US regulatory action and the SEC rather than any technical underlying reason for why it should or shouldn’t be. Regardless, none of this is relevant any longer with the emergence and proliferation of projects that have revenue-sharing models and balance sheets that clearly indicate equity-like token structures and doing so very successfully (although many point to a loophole regarding token holders having to do ‘work’, i.e. staking, in order to share in the profits and thus passing the Howey Test). Therefore, we can evolve beyond just the Fat Protocol driven value thesis and also determine the value of a token by the revenue and cashflow being distributed back to token holders.

How staking rewards transfer value from the network effects of the Terra blockchain to the Luna token is self-explanatory. However, something that commonly gets overlooked is that Terra is the only blockchain where network security is fully incentivized by on-chain transaction fees without the need for staking token inflation. Inflationary rewards to miners or validators are common, from Bitcoin and Ethereum to other emerging blockchains such as Cardano and Solana. The benefits of non-inflationary rewards are obvious, where dilution of supply is a negative value trait.

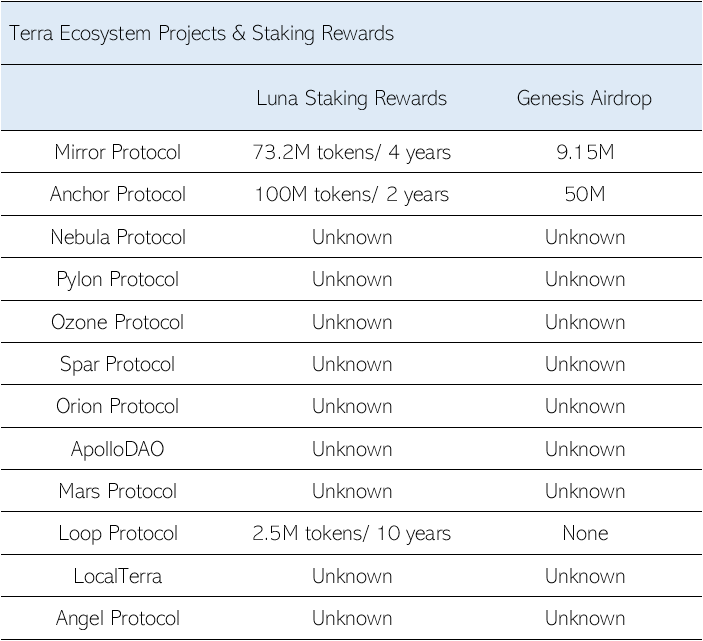

Another aspect of staking rewards not common to other PoS blockchains are the regular or irregular (genesis) “air-drops” that are distributed to Luna stakers. Normally air-drops are a marketing stunt to promote awareness of new projects but a more common way of recent it is being used is to reward and engage the userbases of other protocols/ applications to bootstrap a community of token holders and protocol users. For the two core Terra projects created by TFL, Mirror and Anchor, this has been a significant portion of regular (in this case, weekly) staking rewards sustaining for the next 2 to 4 years (a large genesis airdrop also existed at launch for each project.

These regular airdrops are so significant that the staking APR almost doubles from 9.8% without any airdrops to ~18% with them. What is notable is that this mode of rewarding and engaging Luna stakers through airdrops by Terra dApps, started by TFL, has inspired the next wave of Terra ecosystem projects to do the same. Every project listed in Table 1 below has acknowledged that their tokens will be airdropped to Luna stakers and with almost 90% of new and currently known projects (with tokens) issuing an airdrop bodes well for this trend to continue as the ecosystem expands (with as many as 100+ projects currently building on Terra). As such it can be assumed staking rewards will significantly increase in proportion to the growth of Terra’s application layer, not only with network transactions but, with airdrops.

Seigniorage Induced Deflation

It has already been explained how Terra stablecoins such as UST are minted. It’s easy to then see how increased use-cases and demand for Terra stablecoins will generate deflationary properties in the token supply, inherently increasing its value.

In traditional equities, this type of supply burn would be called a buyback, a common way of distributing profit back to shareholders. This mechanism is also becoming common within cryptocurrencies, most notably in centralized exchange tokens such as Binance and FTX coins, BNB and FTT respectively.

As shown in the Table 2 above, Luna’s supply burn is almost 2.5 times larger than BNB’s which is currently the third largest cryptocurrency by market cap.1

The supply growth of UST (TerraUSD) is the clearest example of demand for Terra stablecoins and Luna supply deflation. Use-cases for UST were non-existent until the launch of Mirror in December 2020 and then Anchor in March 2021. From these two applications UST has catapulted in market capitalization from nothing to $2B, becoming the 5th largest stablecoin and largest algorithmic stablecoin whilst only having liquidity on 8 exchanges compared to Tether’s 361.

The Terra ecosystem has just begun, with only two apps in operation kickstarted by the TFL team but as listed in Table 1 the second wave of dApps is currently being developed.

The Fat Octopus Protocol

So, we’ve talked about how Luna accrues value from increased demand for Terra stablecoins through the various existing and upcoming number of Terra dApps. However, what is unique about Terra is that Terra assets and its dApps aren’t confined to just exist and operate on the Terra blockchain. In fact, the founding team encourages cross-chain composability, evident in the Ethereum version of the Mirror dApp with Mirror assets existing both on the Ethereum and Binance Smart Chain blockchains.

*Pancake Swap data is out of sync so extrapolations have been made to approximate current trading volume

Table 3 above shows TerraUSD (UST) volume by blockchain and it’s notable that volume is actually the lowest on Terra. With the arrival of Solana Wormhole, Terra assets will exist on Solana and will soon exist on other Cosmos SDK blockchains via the Inter-Blockchain Communication protocol (IBC). There were also early indications of the Anchor protocol being deployed on Polkadot via the Interchain Asset Association.

This is where the Fat Octopus Protocol thesis comes in, a modification of the fat protocol developed by Joel Monegro. Because Terra stablecoins and other Terra assets can comfortably exist on other blockchains and non-Terra-based applications we can see that the Luna token will not only capture value within its own protocol, but other protocols too, hence the Fat Octopus.

Terra’s competitive offering is not as a more technologically advanced blockchain, especially considering many blockchains are developed using the same Cosmos SDK. Although, Tendermint consensus is a great foundation for DeFi and payments focused platforms with ~1,200 TPS and low fees and therefore many Terra applications will build on Terra. However, layer 1 smart contract blockchains are still in its nascency with technological innovation continuing and large networks developing especially around Ethereum. The prime and central offering of Terra is the better form of money that is immutable, censorship-resistant and useful.

It is the vision and ambition of Terra for Terra stablecoins to become the most dominant stablecoin as the only cross-chain, decentralized and commercially successful one. Luna can therefore be considered a chain-agnostic bet on the future of decentralized Terra stablecoins, whether it’s a multi-chain or an Ethereum dominated world.

TFL’s Developer Relations, Will Chen, encapsulates this vision in his tweet below.

2. The Case for Terra Stablecoins

Having the infrastructure in place for Terra stablecoins to exist on other blockchains is convenient but that in itself doesn’t determine a market. It’s evident that there is strong demand for TerraUSD from the other two blockchains that house it as seen from the trade volumes in Table 3 and other non-Terra-based apps like Pancake Swap and Curve.

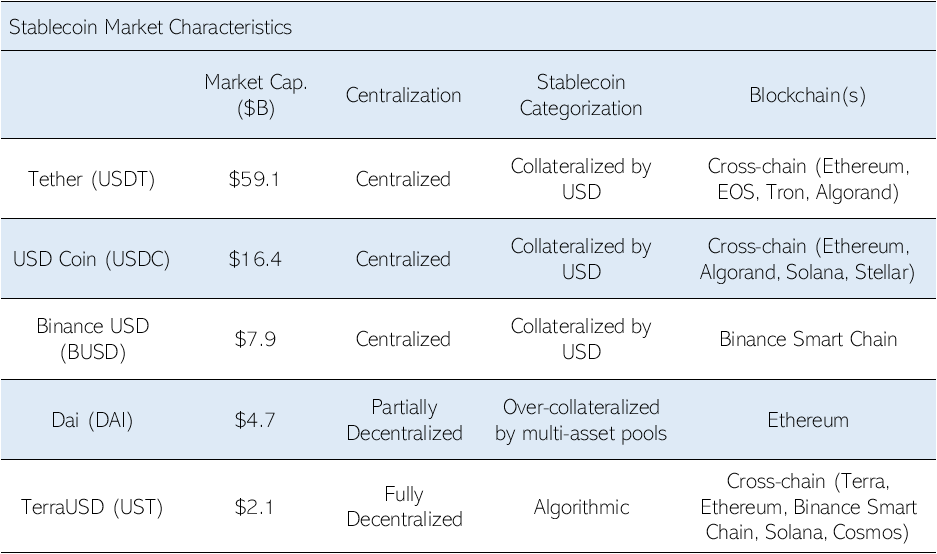

Before we explore the value propositions of Terra’s offerings, let’s look at the stablecoin market. There are now established stablecoins that have dominated the market since the inception of the concept, primarily Tether (USDT), USD Coin (USDC) and Dai (DAI). The concept and usefulness of stablecoins has been well-defined in the likes of The Block’s 2020 report2 and are considered by many as the “killer-app” for cryptocurrencies. They can be faster and more cost effective compared to traditional banking infrastructure with settlement occurring within a minute with probabilistic finality and fees generally being far lower, depending on the underlying blockchain.

Centralized Stablecoins

Tether, USD Coin and Binance USD are fiat-collateralized stablecoins and are pegged to the USD by a centralized issuer and maintained by 1:1 backed reserves (however controversial). Centralized stablecoins have advantages in capital efficiency, redeemable for fiat, assured peg and active regulatory maneuvering by the issuer. Tether in particular has been mired in controversy ever since its inception with little to no transparency around its reserves and many questioning its legitimacy. A summary of significant events surrounding Tether have been as follows:

April 2017 – Bitfinex, the issuer of Tether, was cut off from its banks and Tether’s $1 peg broke for the first time

December 2017 – CFTC issues subpoenas to Bitfinex and Tether3

October 2018 – Questions about Tether’s solvency resurface resulting in the peg breaking down and trading as low as 5% below it for three weeks

January 2020 – The State of New York issues a lawsuit against Bitfinex and Tether for market manipulation

Allegations and controversy surrounding Tether have been so serious that many so-called pundits have suggested that the Bitcoin and cryptocurrency markets have been manipulated and ‘propped up’ by unbacked Tether issuance4. Despite these serious ongoing allegations the purpose of this report is not to discredit the legitimacy of Tether and its reserves, but to show the inherent risks with centralized stablecoins from regulation, blacklisting of users and the peg itself depending on the trust of centralized issuers and their management of reserves.

Decentralized Stablecoins

In this context it’s clear that censor-ship resistant, permissionless and immutable stablecoins would have several advantages over its centralized counterparts. Decentralized stablecoins align with the ethos of Bitcoin and has the same beneficial properties. There are currently two categories of decentralized stablecoins: (1) over-collateralized by multi-asset pools, and (2) algorithmic.

Dai falls into the first category and has achieved considerable adoption within Ethereum as a decentralized stablecoin with many DeFi dApps providing useful utility for it. However, being over-collateralized comes with one major flaw. In order to mint/ borrow Dai one must provide collateral of at least 150% of the value of the Dai being minted. Not only is this extremely capital-intensive but because the collateral is denominated mostly in Ethereum, a hyper-volatile asset, Dai is and has been extremely vulnerable to crypto- market-wide shocks. This vulnerability was most prominently exposed in March 2020 during the market wide crash which saw extreme volatility in the value of Ethereum resulting in liquidations of most of its collateral debt positions and breaking the Dai-dollar peg by as much as 22% (according to Coingecko).

This flaw also relates to why Dai has been categorized as ‘partially decentralized’ in Table 4. As noted above, during periods of extreme market volatility Dai has struggled to hold its peg. To avoid this MakerDAO has allowed up to 40% of existing Dai to be collateralized by USDC, a centralized stablecoin. Following the extreme market volatility in May 2021 a governance proposal was raised and passed, to increase the USDC collateralization rate to possibly more than 50%. In such a scenario it is not factually correct to label Dai as a decentralized stablecoin where a majority of it is in fact ‘backed’ by a centralized one.

TerraUSD falls into the second category and avoids this major flaw by not having to monitor collateral positions and the peg being maintained by efficient markets. However, TerraUSD is not without its own flaws and had its first real stress test during the same extreme market volatility in May 2021, drifting from its peg to as low as $0.86 (according to Coingecko).

This occurred as on-chain redemption capacity (limit of $20M at 2% spreads) was insufficient to absorb the cascading sell pressure (amplified by liquidations on Anchor) especially as spreads expanded. A proposition, Prop 90 which has already passed governance, looks to increase on-chain redemption capacity up to $100M at lower spreads which would alleviate any future cascading sell pressure from Luna on the UST peg significantly. More information can be referenced from this TFL twitter thread but any concerns about a ‘bank run’ are not valid as Luna does not explicitly collateralize UST, where UST may have some claim on the Luna underlying.

There are definitely new and innovative algorithmic stablecoins appearing, seemingly weekly, that have the potential to improve upon Terra stablecoin offerings. However, a majority of them exist only on the Ethereum chain, are yet unproven and serve no major use-cases, failing to create demand and usefulness which can ultimately lead to fiat-peg instability in extreme cases (see Fei). TerraUSD also has the first mover advantage for decentralized, cross-chain stablecoins, an advantage that Tether has proven to be formidable considering the infrastructure building around such stablecoins becoming increasingly difficult to change over time.

Thus the most significant advantage that Terra stablecoins has over other emerging algorithmic stablecoins is that they are proving real commercial success. This leads on to the third and final value proposition for Terra stablecoins and the ecosystem.

3. Vision and Execution

Big ambitions and ideas are only parts of the recipe for success, and many have failed even with them. Terra and the TFL team have shown the vision, meticulous planning and forethought for how the ecosystem will grow and this is proven in the precision of their execution. Execution is a very broad term, but in this context is used to define the following 2 simplified core developments:

Technological development – ability to execute successful and innovative technological developments

Business development – ability to develop a market around a new technological development whether that be through integrations, enterprise partnerships, marketing, regulatory and legal, and building or supporting focused consumer-facing businesses etc.

One without the other is a recipe for mediocrity and the saying “build and they will come” is flawed as we see with so many startup failures. For cryptocurrencies in particular, lacking moats and full of fast competition, building communities and integrations for actual use of even a technologically advanced protocol is fundamental to its success.

Terra’s original vision for the eco-system has been carefully orchestrated to be outwards-looking and mainstream consumer-focused with the user experience first in mind. Many of the existing successful projects within crypto are instead inwards-looking, aiming to solve problems and add utility to crypto-assets for crypto-native users. Ultimately for Terra, it is the goal that the end user doesn’t or won’t have to recognize they are interacting with blockchain technology, much like many modern-day users of the internet have little comprehension about HTTP or TCP/IP protocols for example.

Currently, crypto-native users are significantly more technologically adept than the average person and this is proven simply through their ability to use and custody their own wallets and interact with DeFi protocols. The market for this userbase is extremely niche. However, Terra’s focus on building out the application layer and abstracting away the complexity of blockchain technology from the end-user dramatically expands the total addressable market to essentially the entire global consumer financial market.

The ultimate example that embodies both Terra’s ability to execute at an extremely high level and its ambitious vision is its first project and application, Chai.

Chai

Chai is a payment platform, leveraging the Terra blockchain and aiming to provide the lowest-in-market transaction fees to merchants and various, dynamic benefits to consumers. The value proposition to both merchants and consumers have been clearly defined such that it is preferred over traditional payment infrastructure.

For merchants, Chai and Terra as a payment rail allows 0.5% transaction fees and <6s transaction times. This is a significant efficiency gain on the part of merchants considering legacy payment transaction fees can be as high as 3% with settlement taking up to days.

For consumers, the primary incentive for using Chai has been discounts that are subsidized by TFL as a share of the seigniorage revenue gained from the minting of Terra stablecoins. This incentive may seem unsustainable especially with seigniorage rewards disappearing, but the truly more significant incentives will come with direct integrations into other Terra dApps like Anchor’s 20% savings rate and decentralized Mirror asset investing for the entire Chai userbase. Chai’s operations are centralized as should be for a frontend company requiring enterprise level integrations with regulatory approval. Its workflow, simplified, is as follows:

Consumer ‘Alice’ connects her bank account with the Chai app

Alice makes a purchase using Chai

Chai creates and manages a wallet on behalf of Alice

Chai uses Alice’s KRW (Korean Won) to purchase KRT (TerraKRW) on her behalf

Chai sends Alice’s KRT minus the transaction fee to the merchant’s wallet

Chai launched in June 2019 and currently only operates in South Korea and Mongolia but with plans to expand into the rest of Asia. Chai is an independent entity, initially stood up by TFL and is not a dApp by conventional means. It also facilitates transaction fees at cost or a slight loss with most of the transaction value being captured by the Luna token (payment companies do not conventionally make significant revenues from transaction volume and are rather valuable as strategic infrastructure to build on top of the userbase).

This is all to say Chai’s execution and growth have been nothing short of amazing, especially for a crypto-based company. Chai has been able to partner with some of the largest enterprise consumer franchises, conglomerates and shopping centers in the country with 2.5M users5. Chai claims that the partnership alliance with eCommerce and retail platforms amounts to a total of 45M users and $25B in GMV (Gross Merchandise Value).

With almost 5% of the entire population of South Korea using Chai, it is the only example of widespread mainstream adoption and evidence of disruption of incumbents by a crypto based protocol.

A major argument for centralized stablecoins is the perceived regulatory advantage they have in advancing and securing enterprise-level integrations. This can be seen as recent as Visa’s recent announcement about settling transactions using USDC. However, it’s clear examining Chai as a case study that proves even a decentralized stablecoin can achieve enterprise-level integrations with full regulatory approval in a first world country.

The Mirror and Anchor Protocols (further information linked) are the second and third apps developed by TFL which again have both seen immense success since launching. Anchor is another clear example of an outwards focused vision with the goal of becoming the “Stripe for savings” and we are already seeing evidence of non-crypto-native fintech companies integrating Anchor savings.

The Terra ecosystem expansion and its Cambrian explosion is now just starting with the foundations laid by the team with its 3 core applications: Chai, Mirror and Anchor.

Now, this is not a genuine comparison as the burn mechanisms differ with BNB/ FTT acting more like traditional equities and Luna via seigniorage burns. But this provides a reference point towards the magnitude at which Luna supply is burning compared to some of the largest crypto exchanges currently operating.

Stablecoins: Bridging the Network Gap Between Traditional Money and Digital Value (2020); The Block Research

U.S. Regulators Subpoena Crypto Exchange Bitfinex, Tether January 30th, 2018.

Griffin, John M.; Shams, Amin (13 June 2018). "Is Bitcoin Really Un-Tethered?". Social Science Research Network.

https://www.chaiscan.com/server/web/Dashboard_selectPage

Excellent article thanks! Would love to read the larger investment thesis paper referred to if you are able to share. 🙏👍