Mirror: Decentralized Investing For The Masses

A look into the Mirror protocol, a decentralized and synthetic asset platform aiming to become the next Robinhood

Disclaimer: The bulk of this report was written in early March 2021 and as such some of data is outdated due to the speed at which Crypto moves (“classic”). This report is also not financial advice and the author of this report owns the $MIR token.

The Mirror Protocol is 3 months old with ~760M in equivalent USD trading volume in the last month and ~980M USD1 equivalent total volume locked within the protocol. Furthermore, not only does the protocol already distribute profits to its ‘shareholders’, it has a 100% propensity to dividend with a 100% payout ratio. These characteristics simply do not exist in the traditional finance and venture capital world where most early stage businesses are unprofitable for many years.

The Mirror Protocol (via $MIR, a governance token) currently has a market capitalization of $270M and is severely undervalued considering its growth, competitors, value propositions, TAM and the ability to return dividends at such an early stage.

Background

Mirror Protocol is a DeFi protocol and synthetic asset platform that allows the creation of fungible assets that reflect or ‘mirror’ the price/ value of real-world assets. Synthetic assets on the Mirror Protocol are called Mirrored Assets, or ‘mAssets’ and allow investors anywhere in the world to gain price exposure without actually owning or transacting the underlying real assets. Some mAssets currently trading on Mirror are mTSLA, mGOOGL and mAAPL which reflect the price of the NASDAQ listed shares of Tesla, Alphabet and Apple respectively. Mirror smart contracts are built on the Terra blockchain, leveraging Terra stablecoins such as TerraUSD ($UST) as the collateral asset.

The protocol launched in December 2020 with a hot start, seeing almost instantaneous uptake after its first month.

Terra is an application-specific blockchain built using Cosmos SDK and relying on Tendermint for PoS consensus. The Terra blockchain has extremely low transaction costs and high throughput while having good interoperability for cross-chain activity. The team behind Terra and Mirror also built the Chai app which is a payment platform currently operating in Korea with 2.3M users, $2M in daily transactions2 and integrated with major retail businesses such as CGV, a national cinema chain. The team has proven the ability to execute and scale projects which reflects well on the potential for Mirror to reach its full potential in the same way.

The Value Proposition

I couldn’t have articulated the value proposition for Mirror Protocol as well as its whitepaper has so I’ve quoted it here instead.

Traditional asset classes have yet to enter the transparent, censorship resistant and globally accessible universe of public blockchains. Geographical barriers, high transaction costs and liquidity constraints make it hard for the average person to invest a small amount in assets like stocks and real estate. Asset tokenization has the potential to break down many of those barriers via blockchain reflections of traditional assets that are globally accessible, infinitely divisible and cheap to transact in … Mirror has the potential to democratize finance by making assets of all shapes and forms accessible to anyone, anywhere in the world.3

Four major narratives exist for why a decentralized synthetic asset platform needs to exist. The first is that access to transparent and censorship resistant exposure to traditional financial assets such as stocks currently does not exist. The Gamestop saga illustrates this need in the most dramatic way, a widely publicized event that resulted in unjust treatment of retail traders via trading halts, market manipulation and opaque and supposedly malicious activity by large financial actors. This event exposed to a wider audience that average traders and investors simply do not have the same access that larger institutions have in investing. In this instance, Mirror would have allowed investors to continue to trade the Gamestop stock, alongside institutions, while many retail-centric trading platforms such as Robinhood and Fidelity restricted their own users.

Another such disadvantage that retail traders have is the inability to access trades outside of normal trading hours, a privilege that most institutional and sophisticated investors have. It has been argued that momentum profits on stock markets accumulate entirely overnight4 and events do occur outside of market hours. Mirror assets trade 24/7, a function critical in ensuring markets efficiently reflect their true value and a benefit that should be accessible for everyone.

Second is the prohibitive costs and general inaccessibility of ownership of financial assets such as stocks, bonds, derivatives and illiquid assets. This is especially more pronounced for unsophisticated investors outside of the U.S. Mirror Protocol provides a fair and equitable foundation for individuals around the world to have greater access to financial assets without the need for high capital and prohibitive requirements.

Third is the unique investment and hedging opportunities that unregulated and decentralized synthetic assets provide. Derivatives of any form could potentially be created as long as reliable and decentralized oracle feeds exist. The potential range is unbound for example, fractionalized ownership of real estate or fine art, or synthetic assets that reflect Ethereum gas fees which can be used by miners or traders to hedge gas usage.

Finally, Mirror presents unique opportunities for excess yield on equity and other synthetic asset investments beyond capital appreciation. What’s possible in terms of yield bearing equity assets is a completely new financial phenomenon and its potential and attractiveness as a financial product is limitless, not only to the average investor but also to institutions. Simply, mAssets can currently be deposited into liquidity pools for excess yield in the form of $MIR APR in the range of 100-200%. In the future, these same mAssets could also be deposited into money markets to gain further yield or liquid staking could provide ample liquidity for those same yield bearing mAssets. In any case, a yield bearing equity is certainly an interesting concept that even larger financial institutions could find value in and if that were the case, the total addressable market could be significant.

The Protocol Mechanism

Mirror Assets are ‘minted’ and created in a decentralized manner by users of the protocol by depositing and locking up >150% of the current asset value in Terra stablecoins (e.g. TerraUSD) or other mAssets as collateral. If the value of the asset rises above the collaterization threshold, the collateral is liquidated to guarantee solvency of the system. To ‘mirror’ the price of the underlying asset, the protocol reads prices via the Band Protocol, a decentralized data oracle, every 30 seconds. When the price of the mAsset drifts significantly from the primary market, arbitrageurs are incentivized to purchase/ sell the asset to mint/ burn to claim the collateral. To provide sufficient liquidity for each mAsset market the protocol rewards $MIR to liquidity providers.

Mirror Assets are currently available on decentralized exchanges on the Terra, Ethereum and BSC blockchains. Further cross-chain support onto other larger L1 blockchains is possible as made evident by the Shuttle bridge and future transition to Wormhole, a decentralized bridge to Solana. As the Terra blockchain is built on Cosmos SDK it will also take advantage of the Inter-Blockchain Communication (IBC) protocol and the Stargate upgrade. It is not difficult to imagine mAssets tradeable on every major blockchain in the future, further reducing frictions for mass adoption.

The Mirror Governance Token, $MIR

The Mirror Protocol is extremely unique, even within Crypto, in the sense that there is no one legal entity that owns and is liable for it. All the tokens were initially airdropped to the community as per the distribution schedule below. The protocol is truly decentralized and governed so, not only inherently as a protocol on a public blockchain but no tokens were explicitly allocated to the team or developers.

Whilst the team behind Terra built the Mirror Protocol, the on-chain treasury and code changes are fully governed by $MIR holders, of which the Terraform labs holds none. There are also no admin keys or special access privileges granted.

This presents a myriad of benefits, but most importantly no regulatory liability exists which is critical for a protocol that potentially skirts financial regulations such as absent KYC of its users. There is a planned total of 370,575,000 $MIR tokens to be distributed over 4 years and no more tokens introduced beyond that to the supply.

Currently the $MIR token serves two purposes, as a governance token to vote on/ raise proposals and to collect fees, called rewards, from the protocol. A 1.5% protocol fee is generated from closing CDPs (Collateral Debt Positions). These fees are then sold for TerraUSD to buy $MIR and distributed as rewards to $MIR stakers in proportion to the percentage of the total stake. This process balances the generation of new $MIR by creating buying pressure.

Competition

Other Synthetic Asset Platforms – Synthetix

Synthetix is a direct competitor to Mirror, also a synthetic asset platform built on Ethereum. However, there are key differences between the two platforms, some of which are listed below:

Chain characteristics

As Synthetix is built on Ethereum, settlement times can take anywhere between 14 seconds to hours depending on the gas fees paid. Gas fees can also be as high as $30 during periods of high congestion. These factors make it prohibitive for traders that trade with high volume or for the average investor where fees make up a large portion of the investment itself. Synthetix assets can also only be traded on its own platform and confined to the Ethereum blockchain.

The Terra blockchain allows quick and consistent settlement times (<6s) and extremely low fees (<$0.1). Mirror Assets can not only be traded on multiple blockchains, its trading is not confined to its own platform as liquidity exists on other AMMs such as Uniswap. Mirror Assets are therefore not built on a web-app centralized product but promotes composability and decentralized liquidity for greater access, awareness and adoption.

Fee extraction and reward mechanism

Synthetix charges a 0.3% fee for each transaction and thus scales linearly with trading volume on the platform. However, Synthetix staking rewards are escrowed for 1 year to dampen selling pressure that might occur with inflationary type rewards. Mirror Protocol fees are collected from CDP closeouts which are then used to buy $MIR which creates buying pressure that balances out the inflationary $MIR distribution. This means that the Mirror fee structure is not linear to trading volume or AUM/ TVL.

Minting mechanism

Synthetix requires its governance token $SNX as collateral for minting new assets and due to the volatility of the token it has a 750% collateralization ratio requirement. The Mirror Protocol uses Terra stablecoins as collateral and thus only requires a 150% collateralization ratio requirement, providing a significantly more capital efficient means to minting assets than Synthetix.

While Mirror has only been operating for 3 months, Synthetix has had 2 years to build out its platform since launching. Despite this time difference some key statistics tell a different story:

Only 5 of the assets trading on the Synthetix platform are non-crypto assets and only one, Tesla, is a public equity. This compared to 18 of the assets trading on the Mirror platform consisting of non-crypto assets and 13 of those being public equities.

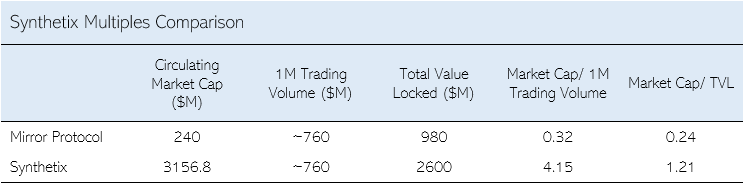

Both Synthetix and Mirror trading volume for the last month was about equal at ~760M USD equivalent.

Synthetix has a total value locked or TVL metric of $2.6B whereas Mirror has a TVL of $980M.

This is not an attempt to discredit the work and innovation that Synthetix has achieved but is a testament to how great the Terra team’s ability is in execution.

Robinhood & Traditional Finance Comparisons

The ultimate vision for Mirror is not to compete within the Crypto space but beyond, into traditional finance and the likes of Robinhood. How Mirror differentiates itself, already defined by the value propositions outlined above, is a non-custodial and far superior onboarding experience whilst providing the same familiar and easy UI/UX. Via the Mirror Wallet mobile app, Mirror allows users to onboard in just seconds, without any registration with direct USD deposits via Moonpay or Terra stablecoins.

Valuation

Multiples Comparison

Synthetix

As a direct competitor, Synthetix provides the most apt comparison. Fair valuations were estimated using the Total Value Locked (TVL) metric and 1-month trading volumes.

Using the Synthetix multiples, Mirror should be valued between $1.2B to $3.2B.

DEXes

Comparisons have also been made using the same metrics for decentralized exchanges (DEX). These DEX protocols do not serve as reliable comparisons but the mechanism of pooling liquidity and allowing trading of those pooled assets remains the same.

Using the average of the multiples, Mirror should be valued between $260M to $1.3B.

Traditional Finance Platforms

Further comparisons can be made with traditional financial platforms, both crypto-native and non-crypto using the sales metric (total revenue from trading volume) and the P/S multiple.

*Based on early IPO valuation estimates

Using the average of the multiples and making assumptions about FY21 sales (in this case, the staking rewards) Mirror should be valued between $1.9B and $2.2B. This implied valuation is based on the bull and bear case trading forecasts used in the DDM.

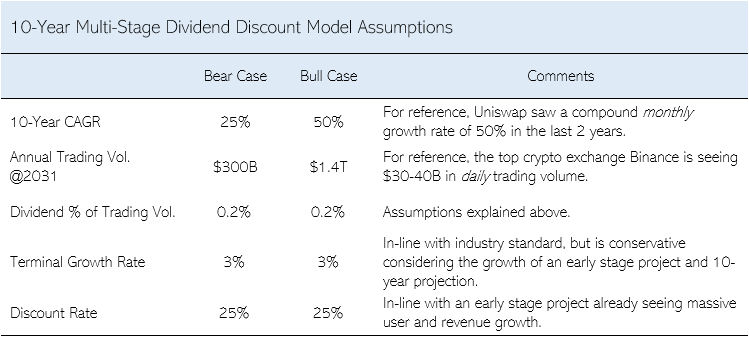

Dividend Discount Model

Broad assumptions have been made for the dividend discount (DDM) and forecasting models due to limited data. For example, the historical data on CDP withdrawal fees and rewards (equivalent dividends) that are issued to $MIR stakers is not available. However, the staking annual percentage rate (APR) has been approximately 30% on average for the month of February on an average total staking ratio of 30%. This results in an approximate dividend of $1.7M for the month of February which approximately represents rewards of 0.2% of trading volume.

It is unlikely that the rewards would continue to have a linear relationship with trading volume, but additional fees could be implemented to create a linear and stable reward structure. Uniswap has proposals in place for a similar mechanism by converting 0.05% of the 0.3% LP reward fee to reward Uniswap governance token holders instead5.

The implied market capitalization of the bear and bull case produced from the multi-stage DDM is $850M and $3.3B respectively.

Mirror Valuation

The implied valuation of Mirror has been calculated on a probability-weighted outcome for each method. Greater weights have been placed on the Synethix comparison, as a direct competitor and the DDM.

The estimated valuation for the bear and bull case is $1.12B and $2.95B and at the current circulating supply of 45M, the implied $MIR token price is $18.8 and $74.0 respectively. This valuation implies an upside of 4.66x and 12x for the $MIR market capitalization for each case.

One caveat is the scheduled dilution of the $MIR token over the next 4 years as per Fig. 4 such that the full upside would not be reflected in the capital appreciation of the token itself. However, the dividend rewards and evolving mechanics have the potential to continue to support appreciation of the $MIR stake of existing holders along with the market cap.

Opportunities

Value Accrual & Utility Functions

Value accrual methods could expand beyond the current staking rewards. The Mirror document itself states that in future iterations the governance token will serve further purposes for the protocol that increase its utility and value.

The flexibility of token value accrual mechanisms is proven throughout other Crypto protocols, most notably by Ethereum which is planning to implement the Ethereum Improvement Proposal (EIP) 1559. Currently the ETH token is used as gas fees for the network that accrue to miners rather than the token. EIP 1559 introduces a mechanism of sending that gas fee to the network itself as a “burn” called the basefee. This burn acts as a buyback and builds deflationary properties into the ETH token, accruing value proportional to activity on its network.

With the advantage of lower transaction speeds, lower gas fees and zero trading fees it is likely that a majority of trading volume will continue to occur on the Terra blockchain which should present greater opportunities of value capture for the $MIR token. Applying a % trading fee much like Synethix could be easy to apply if low enough as to not dis-incentivize trading. Proposals like these could be implemented via governance in the future.

Another great example is the Uniswap protocol and its governance which currently has no reward mechanism but is valued at almost $15B. Ultimately, valuing the Mirror Protocol by extrapolating its current fee reward mechanism is a disservice to the ingenuity of the platform and the team behind it. Buying Mirror is a bet on the future capabilities and other reward mechanisms that bring cashflow to the governance token.

Leverage & Other Derivative Tools

Leveraging functions and other derivative products such as swaps and inverse stocks (when the underlying stock goes up the inverse derivative price goes down proportionally) could be introduced to the platform.

Version 2 Proposals

Mirror v2 is currently in development but a detailed announcement has not yet been made about what it will consist of. Some already known proposals are the introduction of margin trading, limit orders and pre-IPO contracts. These proposals and the benefits and advantages they bring to Mirror users speaks for themselves.

Terra Eco-system Synergies

Terra is planning to launch a myriad of other DeFi products that can synergize with Mirror. One such example is using Anchor, a lending platform which aims to provide a yield-bearing stablecoin , aUSD, as collateral to further decrease collateralization requirements and introduce yield-bearing elements to mAssets. Another example is creating dynamic index funds using mAssets.

Risks

Regulatory Action

The largest risk that a derivatives platform such as Synthetix or Mirror takes on is regulatory action, particularly from the SEC and CFTC. The best example of this occurring is 1Broker, a platform that allowed users to trade on financial markets (stocks like AAPL or MSFT, commodities like gold, forex markets etc.).

In 2019 the SEC and CFTC sued 1Broker and its CEO for allegedly violating federal law through a bitcoin-based security swap product. Although 1Broker was a Marshall Islands based broker, jurisdiction was claimed based on allowing US-based users to trade financial derivatives despite not meeting the discretionary investment thresholds required by the federal securities laws. 1Broker was eventually closed based on these charges.

The Mirror Protocol may potentially violate similar federal laws that forced the closure of 1Broker. However, one significant factor mentioned earlier prevents the same fate occurring to Mirror. Mirror is a fully decentralized protocol with no legal entity for any legal matter to be settled, nor sued by US government agencies. In a worst case scenario the internet domain of the Mirror web-app itself could be taken over by civil forfeiture but the protocol behind the domain will continue to function. In such a scenario, mAssets would continue to trade wherever there is liquidity on any decentralized exchange.

Traditional Shareholder Rights Nonexistent with mAssets

Holders of synthetic stocks like mAssets don’t have the same rights as traditional shareholders do in publicly listed stocks. This limitation could potentially prohibit investors from investing in mAssets as the value proposition falls short of the value of the following shareholder rights:

Right to vote and attend AGMs

Right to receive annual reports and access financial records

Right to receive dividends

Right to ownership of the underlying equity

Let’s visit each set of rights as an mAsset holder assuming the mAsset is a synthetic of a publicly listed stock such as mAAPL (the mirrored and tokenized version of NASDAQ: AAPL):

Investors of mAAPL will not have shareholder rights to vote and attend AGMs. This is made less impactful as retail investors/ traders would normally have an insignificant share of the total shares outstanding such that votes would be insignificant. This is further emphasized by the fact that stocks voted in via governance would normally be large cap, highly liquid stocks that further diminishes the disadvantage an investor would have by holding the synthetic version of a stock in terms of voting rights.

Investors of mAAPL would still have access to financial records and reports as these are all made public as per SEC regulations.

Investors of mAAPL would not receive dividends that AAPL shareholders do. This may initially seem a significant disadvantage, however dividend yields have been steadily decreasing over time and is no longer the common way of rewarding shareholders. Instead, buybacks have been the preferred method of distributing profits and this benefit is shared equally with mAsset holders as it is reflected in an increase in the share price. The other factor is that mAssets can deliver yield in other forms, as mentioned already, that could be significantly higher than traditional dividend yields. The S&P500 dividend yield is currently around 2% whilst the mAsset LP rewards have APRs higher than 100%.

In a liquidation or sale resulting in transfer of ownership, shareholders would have claim over a proportion of the equity. In such a bankruptcy event, investors of mAAPL would not see any equity and it is unclear how the Mirror Protocol would handle acquisitions if the mAsset is the acquired or liquidated company.

Finite Treasury For Further Development and Support

Currently Mirror has a sizeable treasury, funded by the initial airdrop, currently at 36.5M $MIR (~$230M USD). This is sufficient for a new project and no serious concerns exist for its continuing operations for the foreseeable future. There is also potential for this to grow considerable with $MIR price, but on the flipside risks are present with the entire treasury being held in the form of its own governance token. If the protocol sees headwinds in the future, this could be reflected in the $MIR price and its treasury size.

Even with massive drawdowns in the Mirror treasury it is in the Terraform Lab’s interest to continue to support the protocol. While the Terraform Labs would not capture direct upside from the success of Mirror, it provides significant secondary value accrual to the Terra blockchain as made evident by the massive increase in demand and subsequent market capitalization of TerraUSD ($UST) since Mirror was launched in Dec 2020.

Oracle Limitations

Oracles in general are prone to failures during black swan financial events and potentially vulnerable to exploitation. Although no significant failure event has occurred to note.

Mirror is currently using the Band oracle only which is a relatively smaller and newer protocol which creates a single point of failure and unforeseen risks such as quality and accuracy of price-feeds.

The Mirror team have confirmed that they plan on diversifying their oracles in the future which should relieve both risks mentioned above.

Conclusion

Mirror is certainly an ambitious project aiming to compete in a sector with growing giants from Synthetix to Robinhood. As a 3-month-old project, already a leader in its space and version 2 on its way there is a lot to be excited about. In the short term there is considerable upside as it appears severely undervalued compared to its competition both in Crypto and outside of it. In the long term, the potential in such a large addressable market is significant as the protocol continues to develop, adoption accelerates, and further value accrual mechanisms are designed and implemented.

TVL and trading volume figures from mirror.finance dashboard and also include estimated figures from Binance Smartchain activity – 10 March 2021

https://www.chaiscan.com/

https://mirror.finance/MirrorWP.pdf

Vasiliki A. Basdekidou. (2017). The Overnight Return Temporal Market Anomaly.

https://uniswap.org/blog/uniswap-v2/#path-to-sustainability; Protocol charge mechanism

Great article! It goes really deep into the subject whilst keeping it clear and easy to understand. Looking forward to more posts like this one. Excellent work.

Thank you so much for you work. This is incredible.

I love learning about Terra ecosystem projects, and blockchain projects in general.

Currently, valuation metrics have been intriguing, since how do we valuate this new asset class of network effect companies?